Trade the Upcoming Results | Quantsapp

Options being the instrument pricing in expected volatility will become more expensive ahead of the event of a corporate result , thus being a volatility indicator.

SHUBHAM AGARWAL | 09-Oct-21

Reading Time: 3 minutes

undefinedAfter completion of the second quarter of the financial year 2021-2022, the quarterly results season has started. The developments thus reported would generally have enough raw material in them to create momentum in the stocks declaring results. We traders, being momentum chasers often times find opportunities to make money from this.

The size of moves could be big enough to give us the opportunity to make money, but with results, the direction is usually more uncertain than usual. So, the surprise that brings in the move could be positive or negative.

Trade betting on a positive surprise with a future or position in equity stock could run into big trouble if the result comes up with a negative surprise.

Here we need a trade that has limited punishment despite being proven grossly wrong yet has open profit potential in case we are proven right.

Options fit the bill well. Such a case in favor of options for an event-like result is widely known and accepted but due to certain inherent characteristics of options thru such event-like results, many of us might not have been able to get the full potential of options.

Let us dig deeper into this character and find a way to deal with it so that we can trade results much more efficiently with Options.

Now, as the Result Calendar date comes closer, the uncertainty element rises. Options being the instrument pricing in expected volatility will become more expensive ahead of the event of the result.

We need to accept the fact that we are buying something a little more expensive than usual. Typical Call/Put premium could be easily 30-50% higher than usual.

At the same time, the second aspect of this is that once the result is announced, the uncertainty is over. As a Company Results , the Premium that rose led by the event of result drops post the event of the result.

To trade results efficiently now we have the change instrument to Options so that negative surprise does not punish us at the same time trade Options with a provision for such post-event fall in premium so that the positive surprise yields us the most possible gain.

To get the best out of the positive surprise there are the following 2 strategic trades. We can choose either one of them that best suits us.

1. Convert the Buy Option trade into a Spread

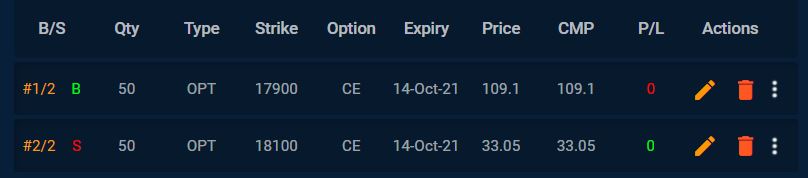

A spread is basically a Buy and Sell position in the same kind of option (Call/Put) in the same Stock or Index. For us, we will keep the expiry also the same. To create such spread if I Buy a Call/Put (depending upon my view), I will simultaneously Sell higher Call/ Lower Put.

For Example: For a stock trading at 100

Buy 100 Call

Sell 110 Call

110 is the point till which we are expecting the stock to move up to post the result. Profits in such a trade get limited to the move up to 110 (as post that every rupee made in 100 Call will be evened out by rupee loss in 110 Call (sold).

However, the good thing is that we are partially immune to the fall in premiums post-event. Also, this trade is inexpensive than the single Call, which makes more sense in times of inflated option premiums.

2. Back Ratios

Once again a trade which is in favor of volatility, here we would Sell the Call/Put that we were going to Buy and Buy 2 lots of relatively closer higher Call/ Lower Put

For Example: For a stock trading at 100

Sell 100 Call

Buy 2 Lots of 102.5 Call

Now this keeps the profit potential open in case if there is violent move expected which could take the stock to 120-125 and one does not want to limit the profits at 110. So, our profits would be open to whatever move one sees above 102.5 minus 2.5 (Loss on 100 Call Sold up to 102.5 as post 102.5 one of the two calls which will compensate the loss on 100 call post 102.5) and the premium outflow while creating the trade.

In both cases in case the volatility does not come along, and the stock sees limited movement, these trades will still outperform the single options.

Good thing in both above trades is that in the event of us going wrong we will outperform just a single bought option. So, from a clear Risk Vs Reward perspective, we are outperforming the Single option. Check Live NSE Results & we provide Analyzed Quarterly Results date to track Live Results.

Learn and read more about short term from Quantsapp classroom which has been curated for understanding of option strategy from scratch, to enable option traders grasp the concepts practically and apply them in a data-driven trading approach.

Recent Articles

Before you buy an Option, ask these 5 questions: Shubham Agarwal

01-Aug-26

Debit spreads vs naked option buying: Shubham Agarwal explains the better strategy in event-driven markets

25-Jul-26

Shubham Agarwal explains where traders go wrong during earnings season

18-Jul-26

When headlines matter more than trends: Shubham Agarwal

11-Jul-26

Why breakout traders must be patient in low volatility markets: Shubham Agarwal

04-Jul-26

When low IV makes option selling difficult: Shubham Agarwal

27-Jun-26

Beyond Price: Finding dynamic support and resistance using Option Open Interest: Shubham Agarwal

20-Jun-26

How to trade gap openings like smart traders: Shubham Agarwal

13-Jun-26

SHUBHAM AGARWAL is a CEO & Head of Research at Quantsapp Pvt. Ltd. He has been into many major kinds of market research and has been a programmer himself in Tens of programming languages. Earlier to the current position, Shubham has served for Motilal Oswal as Head of Quantitative, Technical & Derivatives Research and as a Technical Analyst at JM Financial.

Recent Articles

Before you buy an Option, ask these 5 questions: Shubham Agarwal

01-Aug-26 09:09:00

Debit spreads vs naked option buying: Shubham Agarwal explains the better strategy in event-driven markets

25-Jul-26 08:36:00

Shubham Agarwal explains where traders go wrong during earnings season

18-Jul-26 09:15:00

When headlines matter more than trends: Shubham Agarwal

11-Jul-26 10:18:00

Why breakout traders must be patient in low volatility markets: Shubham Agarwal

04-Jul-26 08:21:00

When low IV makes option selling difficult: Shubham Agarwal

27-Jun-26 10:12:00

Beyond Price: Finding dynamic support and resistance using Option Open Interest: Shubham Agarwal

20-Jun-26 10:16:00